1. Do the concessions actually require the client to retire?

You recall reading that the need to 'retire' depends on which concession is being targeted - the 'premier' 15-year exemption or small business $500,000 retirement exemption.

15-year exemption

If the client is over 55 and has owned the active business asset for at least 15 years, then a declaration of retirement is required to meet the specific conditions of the 15-year exemption1. The 15-year exemption implicitly recognises that the taxpayer has reached the end of the small business road and the sale of the business is part of the client's grand retirement plan.

But what constitutes 'retirement' to gain the exemption? Usually when a client retires, it's a clean break with no intention to resume paid work. This is arguably what the legislation contemplates when it states "in connection with your retirement".

But what if the client, the previous owner, stays on in a consultative role over the following two years for say, a few hours per week, as the new business owner takes over the reins? The ATO acknowledges these commercial realities and would consider the client to have retired for the purposes of the 15-year exemption, even though the client is still 'gainfully' employed (albeit in a reduced capacity). Ultimately, there needs to be evidence of a significant change in work patterns in order for one to be regarded as 'retired'.

$500,000 retirement exemption

If, on the other hand, the active business asset has been owned for less than 15 years, the $500,000 retirement exemption generally can be used as part of the CGT calculation 'reduction process'. The aim of this 'reduction process' is to reduce the gross capital gain using all available concessions including:

· capital losses, if any;

· 50 per cent general discount if eligible;

· Optional 50 per cent active asset relief;

· Optional $500,000 retirement concession; and

· Optional two year rollover.

2. When does the contribution actually have to be made?

So, the $500,000 retirement exemption has a forced contribute rule for under 55s. But when does the contribution actually have to be made?

Recall that the requirement to make a compulsory contribution to super only applies if the individual is under 55 at the time of making the requisite written 'choice' to apply the retirement exemption. Any exempted amount must then be contributed to super by the latter of the following two dates:

1. When sale proceeds are received; or

2. When the client makes the requisite written 'choice' to apply the $500,000 retirement exemption.

This choice could be in the form of a one page hand-written document signed by the taxpayer outlining how much of the lifetime $500,000 retirement exemption is to be claimed. Importantly, though, the choice election is separate to, and distinct from, the client's tax return. This is an important technical point and one that in practice affords the taxpayer an element of discretion as to when, and indeed if, an exempted amount needs to be contributed to super.

3. In-specie contributions and the retirement exemption

If a client under 55 years of age makes an in-specie contribution of business real property into an SMSF, whilst targeting the $500,000 retirement exemption, the requirement to contribute the 'exempted amount' into super (for under 55s) will not be satisfied by virtue of the in-specie contribution itself.

This stems from an ATO interpretation that the actual CGT event, the written choice election and 'forced' contribution cannot take place simultaneously on the same day (which is what one technically requires in the in-specie scenario).

This can be a tricky part of the tax law and requires specialist tax advice to oversee the transaction and/or the attainment of a private binding ruling from the ATO. Ultimately, it means that the client would have to find the cash to make a second follow-up cash contribution of the exempted amount into super. Without a follow-up cash contribution, the conditions to qualify for relief under the retirement exemption will not be satisfied.

In theory, the cash could come from within the SMSF or in the absence of liquidity, within the fund via a short-term limited recourse borrowing arrangement in consideration for the partial acquisition of the business real property from the member.

4. Sale proceeds from the disposal of an active business amount to $1 million

Can a 60-year-old client contribute the entire $1 million in sale proceeds to super and have this attributed to the $1,355,000 CGT contribution cap?

The starting point here is that full use of the $1,355,000 CGT contribution is generally only available if the 15-year exemption is in play. So, if the client in this scenario qualified for full CGT relief under the 15-year exemption, the entire $1 million in sale proceeds could be contributed to super using the CGT contribution cap, assuming they owned the asset solely in their own name.

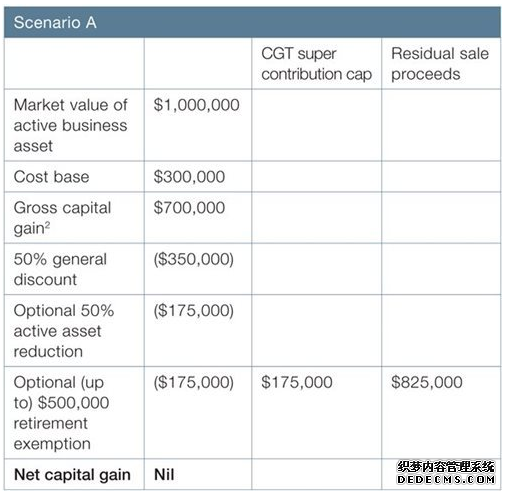

If the 15-year exemption is not in play, then use of the $1,355,000 CGT contribution cap will be limited to the amount of gain exempted under the retirement exemption - the 'exempted amount'. This is an important technical point, so to best illustrate this, let's look at some numbers. Refer to Scenario A.

The first point that needs to be made here is that the CGT reduction process has reduced the $700,000 gross capital gain to nil. This is our primary objective - satisfy the tests that entitle us to apply the concessions to reduce, or totally eliminate, the capital gain.

However, from a super contribution cap perspective, notice how the application of the optional CGT concessions in this particular manner has provided the client with only $175,000 of the CGT contribution cap. In other words, the CGT calculation 'reduction process' has produced an exempted amount of $175,000. If the client intends on contributing the sale proceeds to super (noting that the forced contribution rule doesn't apply because the client is over 55), they will only have $175,000 of the $1,355,000 CGT contribution cap at their disposal.

That leaves us with remaining sale proceeds of $825,000. If the client's objective is to then maximise contributions to super, we need to work within the limits of the non-concessional contributions cap. As a result, this requires careful planning around timing the triggering of the 'bring-forward' rule.

For example, prior to 30 June 2015, the client could contribute $180,000, then contribute a further $540,000 after 1 July 2015. Putting aside any ability to make $35,000 in personal deductible contributions (assuming the client is over 50), in the worst case scenario, the remaining sale proceeds of $105,000 would have to accumulate outside super unless, subject to the qualifying conditions and preservation considerations, the client makes a contribution on behalf of a spouse.

Alternatively, we could hold off from triggering the 'bring-forward' rule until the 2016-17 financial year, after contributing $180,000 in each of the preceding two financial years.

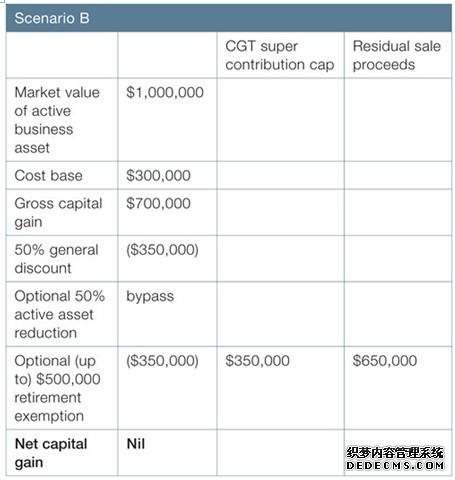

Now consider a different scenario, Scenario B.

In this scenario there is the same asset value and gross capital gain, but a slightly different CGT calculation reduction process is applied.

You will notice that once again we end up with a nil capital gain, but the fundamental difference from Scenario A is that the optional 50 per cent active asset reduction has been 'bypassed'.

The legislation does not force us to apply the 50 per cent active asset reduction and this is an example of when we may want to bypass it as part of the CGT calculation reduction process.

In this particular instance, doing so enables a higher gross capital gain of $350,000 to be 'washed away' using the $500,000 retirement exemption. A higher amount of $350,000 can in turn be contributed into super using the CGT contribution cap (compared with $175,000 in Scenario A). This leaves $650,000 for negotiation with the non-concessional contributions cap.

Again, timing of the 'bring-forward' trigger helps here. The client could contribute $180,000 before 30 June 2015, then from 1 July 2015 contribute the remaining $470,000. In the wash up, the entire $1 million in sale proceeds has been contributed into their own personal super interest within the space of three months.

Other observations

Do not lose sight of the bigger picture here. The primary objective should always be that the small business owner qualifies for CGT relief on disposal of active business assets by satisfying the basic and specific conditions laid out in the tax law. If it turns out that these conditions and tests have been met, then the discussion could extend to the rules that allow sale proceeds to be contributed to super using the CGT contribution cap.

If sale proceeds are intending to be injected into the super environment, strict time frames and administrative guidelines need to be adhered to. For example, the super fund needs to be made aware in advance, or at the time of contribution, that the contribution itself stems from the sale of an active business asset. This is done using a special CGT cap contribution election form (NAT 71161). Also, ensure any necessary or discretionary CGT cap contributions are made within the prescribed timeframes.

In this article, we focused solely on individuals disposing of active business assets. In the real world, assets might be owned jointly (say between husband and wife), so the rules apply to each owner in respect of their share of the capital gain and proceeds accordingly.

From time to time, you may also have clients who have private trusts and/or companies that are themselves disposing of active business assets.

In other words, the CGT event is taking place inside an entity and not in the individual's hands. This arguably introduces an added layer of complexity, given the need for the disposing entity to not only satisfy the strict tests and conditions to qualify for CGT relief in the first place, but also given any desire to push these proceeds out of the operating entity in a tax-effective manner. Nevertheless, expert planning and advice could provide the beneficiaries of these entities with use of part or all of the CGT contribution cap.

The ATO has made it clear that it will take a closer look at any clients claiming small business CGT relief.

Ultimately, the onus is on the accountant to confirm the availability of the small business CGT concessions but if it turns out that the client qualifies, then there are opportunities for financial planners to be involved in the discussion, particularly as attention turns to the injection of those sale proceeds into the super environment using the $1,355,000 CGT super contribution cap (being indexed to $1,395,000 for 2015-16).

Footnotes

1. Note that before even considering these specific conditions, the disposing entity must satisfy an initial set of basic conditions, i.e. active asset test, aggregated $2 million turnover test/$6 million net asset value test and finally the CGT concession stakeholder test (if the asset being disposed are shares/units). If we cannot jump this initial hurdle - the basic conditions - then small business CGT relief is not available and the 15-year exemption becomes a non-issue. Note also that the 15-year exemption also caters for the disposal of active business assets due to a permanent disability.

2. Assuming nil capital losses available.

Small Business Capital Gain Concessions check points

10/16/2015 14:17 visits: